Investing in a uranium mine

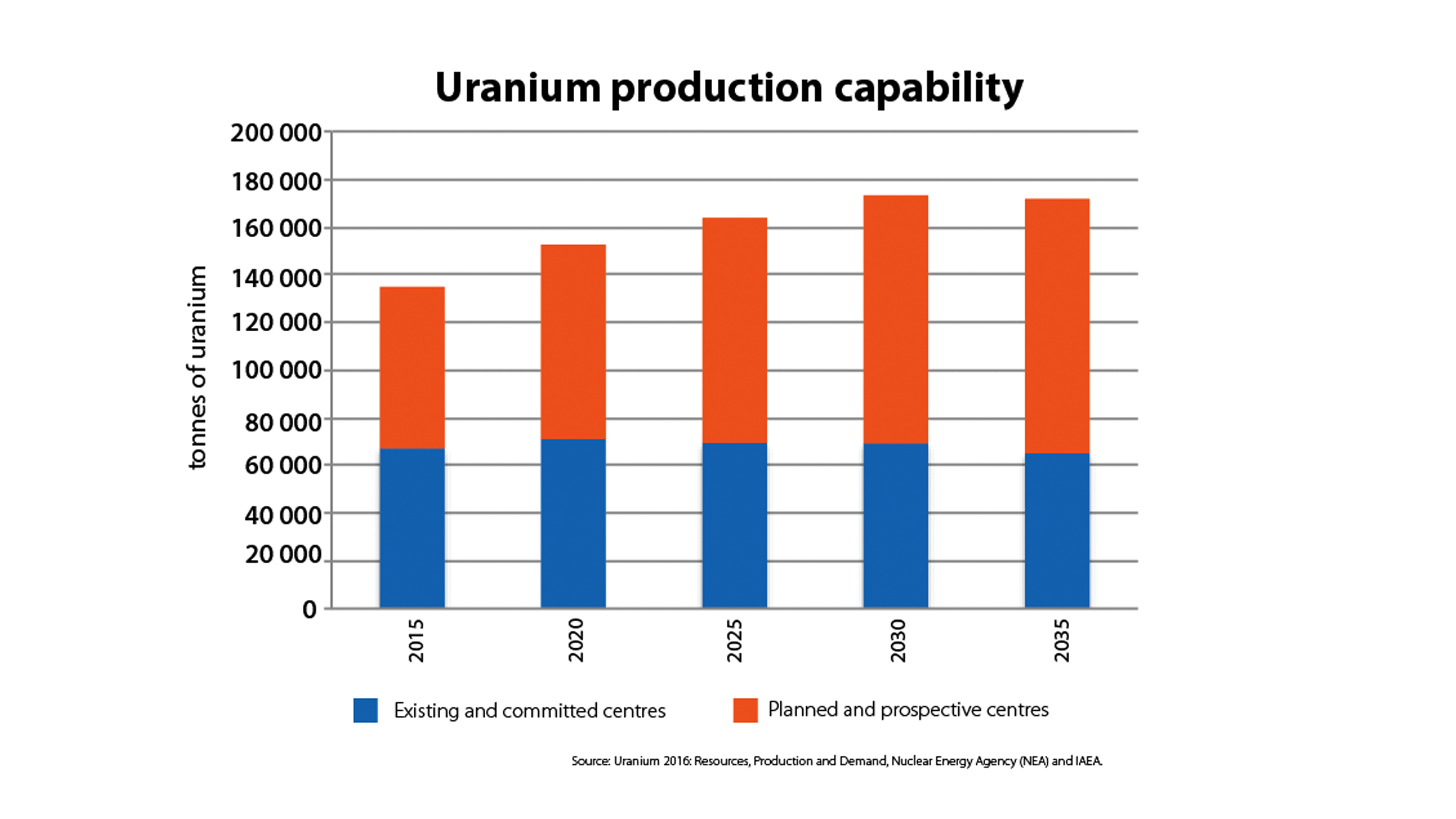

Opening a uranium mine requires significant capital investment and is a long process that often involves 10 to 15 years of lag time before the mine begins operation. The cost of the equipment for mining and milling uranium into uranium ore concentrate, which generally takes place on site, is over US $100 million and can even reach into the billions. Thus, private companies and state entities alike must carefully consider long-term economics before opening a mine. Many countries that are new to uranium mining, such as Botswana and Tanzania, have used the IAEA’s expertise and assistance to create the necessary infrastructure and the legal, environmental and regulatory framework to open mines. The mines are at an advanced stage of exploration, waiting for a more favourable economic environment.

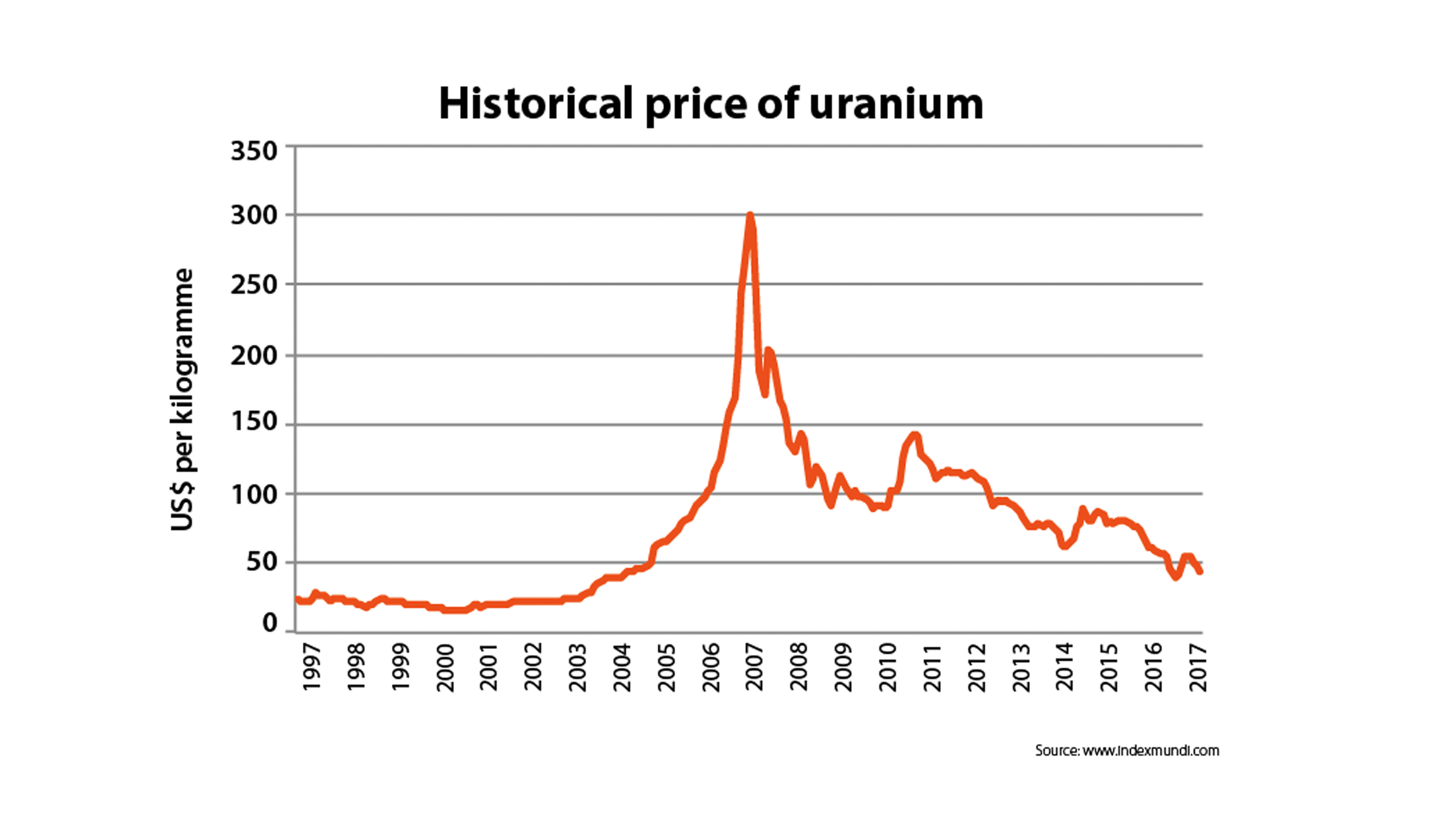

Most contracts in the uranium business are long term, including price ceilings to protect customers and price floors to protect mines. Although spot prices affect the overall market price, this change happens more slowly. Depending on current market price and the level of a country’s nuclear power programme, it can sometimes be more profitable to simply trade uranium than to mine it domestically.

There are countries such as China and India that operate mines mainly to ensure security of domestic supply, with economics being an important but secondary consideration. Most uranium in the world these days is nonetheless mined commercially. Countries like Australia, Kazakhstan and Namibia operate mines for exporting uranium, while others like Canada use the uranium both domestically and for export.

So, what does the crystal ball say? That demand for uranium is forecast to increase in the long run and that prices should increase along with it. But when and by how much is hard to predict, particularly in the light of hesitation by the public in many countries to invest in nuclear power.

“Previous fixes by the industry, through for example strengthening corporate social responsibility or other similar stakeholder engagement efforts, have become less effective given the degree of public scepticism about mineral industries in general,” said Hussein Allaboun, Manager of the Jordanian Uranium Mining Company.

Jordan is one of many countries exploring the prospect of uranium production. It has done feasibility studies and constructed a pilot plant to gather the necessary industrial and engineering data. “The project is envisaged as a constituent in a clustered national nuclear energy transformation programme triggered by the country’s keen need for a secure source of energy,” Allaboun said.